- Immutable: The model cannot be changed or upgraded. It must respond automatically to market conditions, including rates on other platforms.

- Higher target utilization: Supplied assets in Bend are not used as collateral, so markets don’t need to hold large buffers for liquidations. The protocol can target higher utilization and use gentler illiquidity penalties.

The Curve Mechanism

This mechanism resembles the interest rate curves commonly found in traditional lending protocols. The curve is defined by the following features:

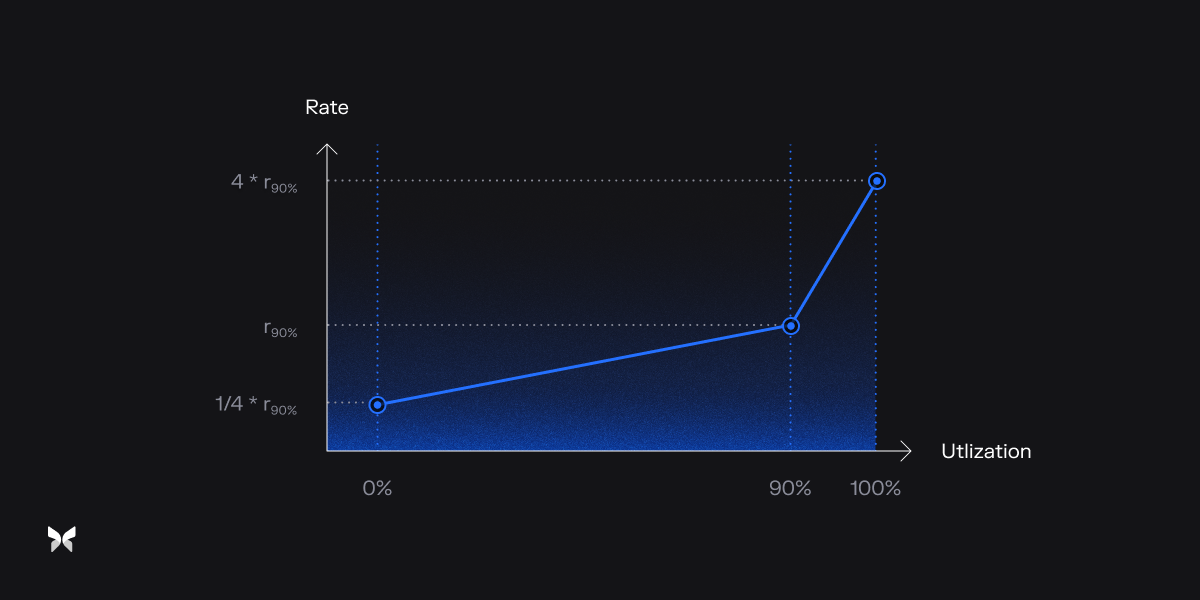

Image provided by Morpho DocsEach time you (or any user) interact with the market—e.g. borrow or repay—utilization changes and the rate updates along the curve. For instance, the following are sample utilization-to-rate relationships:

The Curve Mechanism is designed to respond to short-term fluctuations in utilization, helping maintain healthy market liquidity during periods of sudden borrowing or repayment.

The Adaptive Mechanism

This mechanism continuously shifts the curve to adjust to market conditions over time. The curve shifts over time so the rate adapts to market conditions even when no one is borrowing or repaying.

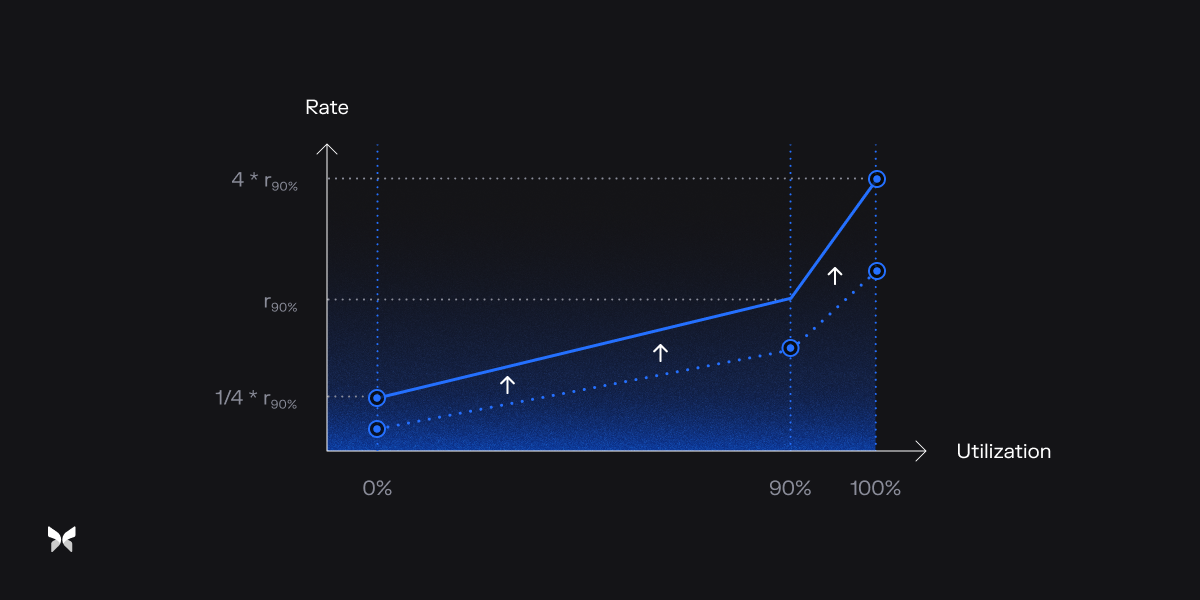

Image provided by Morpho DocsThe adaptive mechanism dynamically shifts the rate curve in response to changing market conditions, even during periods without user interaction. The key value that moves the curve is —the rate at the target utilization. This value gradually changes over time:

- If utilization rises above the target (90%), will steadily increase.

- If utilization falls below the target, will steadily decrease.

Formula breakdown

Utilization

Utilization () is the ratio of total borrowed assets to total supplied assets at time (), with a constant utilization target ().Error

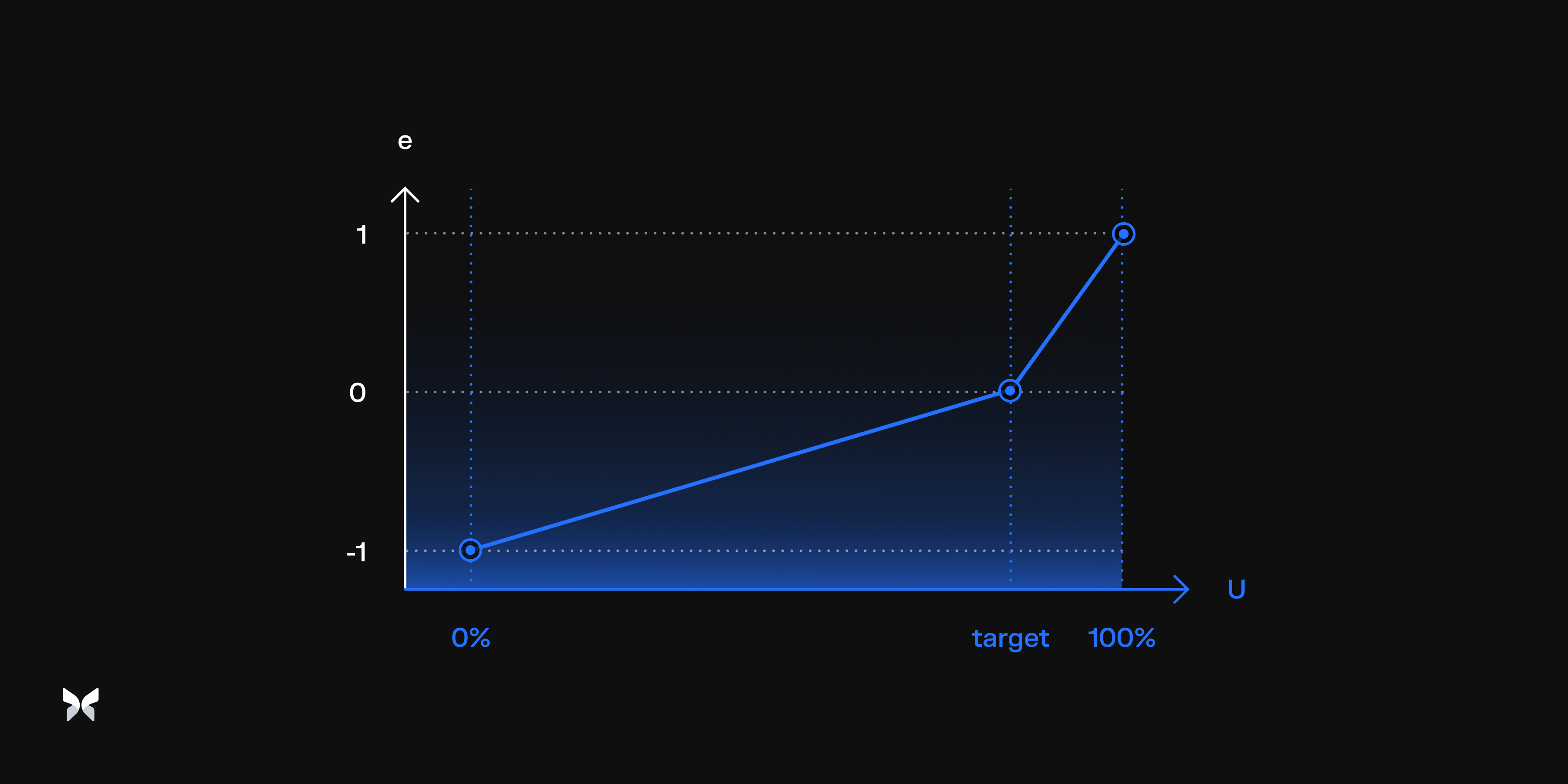

Error () is the normalized difference between the current utilization () and the target utilization (), scaled so that the distance between and equals the distance between and .

Image provided by Morpho Docs

Curve

Curve () determines the shape and sensitivity of the interest rate response to changes in utilization around the target, with different slopes below and above controlled by the constant . withHistory of interactions

History of interactions () represents the set of all past interaction times up to time (), including the initial time (). Noting that the time at which interaction occurred.Last interaction

Last interaction () represents the most recent interaction time before or at time ().Speed

Speed factor () determines how fast the interest rate changes over time based on the error at the last interaction, scaled by ().Rate at target

Rate at target () represents the interest rate when utilization equals the target utilization, evolving over time based on the speed factor. At any time (), the borrow rate () is given by the formula:Calculations

APY is the annualized return for suppliers and cost for borrowers, with compounding. In Bend you use it to compare returns and costs across markets.Borrow APY

The Borrow APY is calculated using the following formula: Where:borrowRateis the borrow rate per second, as determined by the Interest Rate Model (IRM).secondsPerYearrepresents the total number of seconds in a year (31,536,000).

Supply APY

The Supply APY is calculated considering the utilization and the fee. The formula is: Where:feeis the fee of the market on a per-market basis and portion of the interest paid by borrowers that is retained by the protocol. See Yield & Fees for more details.utilizationis calculated as:

Constants

The values of the following constants are hardcoded into the Morpho code deployed on Berachain.- WAD = Wei-based Decimal (WAD = 10^18, meaning 1 WAD = 1.0)